Investment Update 2nd quarter 2020

Stock markets have proved in the past to be surprisingly resilient, bouncing back after major losses every time. But few would have expected stock prices to recover with such fervour after the sharp drop witnessed back in March of this year. In fact, this might seem to contradict the latest economic reports, as more than three months after the global outbreak of the COVID-19 pandemic it is clear this will have a massive impact on the global economy.

Economic outlook: recovery in 2021...

The IMF (International Monetary Fund) estimates that the global economy will contract by an unprecedented 4.9% in 2020. One major difference with previous recessions is that negative growth will not be restricted to the developed world this time around, with average contraction estimated at -8%. Emerging economies are likewise set to shrink (projected average contraction: -3%). Only China is expected to show marginal growth in 2020 – although the growth rate will be markedly lower than the country has experienced over the past few decades.

The ‘good’ news is that the IMF projects that global economic growth will rebound by approximately 5.5% in 2021, with a full recovery to follow during 2022 at the earliest. However, more pessimistic scenarios show a longer road to recovery. Which of these scenarios will eventually materialise will be determined by two factors: 1) how long it will take for a COVID-19 vaccine or medication to become available on a large scale, and 2) whether we will see a second wave of the virus before the vaccine is introduced.

…Or has recovery already begun?

Based on various confidence indicators, however, economic growth is likely to recover before 2021 – in fact, the first stage of growth recovery is already underway, starting in China. After a sharp downturn last February, Chinese business confidence had already snapped back to early-2020 levels by March and has been on the uptick ever since.

Having reached a low in April, confidence indicators in Europe and the United States have largely regained their ground. However, these favourable trends – particularly on the production end – do not mean that economic reports will remain unequivocally optimistic for the foreseeable future. For one, consumer confidence will remain substantially lower than at the start of the COVID-19 pandemic, while unemployment, bankruptcy figures and other data are likely to paint a bleak picture for some time to come.

Financial markets are up

Propelled by unprecedented stimulus measures, the financial markets recovered somewhat during Q2 2020 from the year’s dire first quarter. All asset classes registered gains in the second quarter of 2020, based on what looks like the principle ‘the higher the risk, the higher the return.’ Whereas economic results tend to focus on the performance achieved, stock prices are based on future prospects. Stock markets seem to be optimistic about the future. On average stock prices rose 10% to 20% during the second quarter. Bond prices recovered on the back of the prolonged low capital-market interest rates and the declining risk premiums for corporate bonds and lower-rated government bonds. However, since we continue to record the rise in global infections daily, there remains a risk of write-downs and bankruptcies.

Impact on a.s.r.’s lifecycle returns

The recovery in the financial markets is also reflected in the lifecycle returns for Q2 2020 of the a.s.r. Employee Pension. Equities were the highest-performing asset class. Driven by the strong performance of the tech sector and other variables, US stocks posted a performance of nearly 19%. In other parts of the world, rallies in stocks topped 10%, eradicating more than half of the previous quarter’s losses. Bond prices also rallied, spearheaded by high-yield bonds and emerging-market debt (EMD).

- The returns displayed above have been calculated up to the end up June 2020.

- These returns are net of fund fees and transaction charges, but exclude the investor administration fee charged by a.s.r. Employee Pension.

- The benchmarks for our lifecycles are set on a prorated basis, since all underlying funds have their own relevant benchmarks. For the ASR Amerika Aandelen Basisfonds, for example, this is the MSCI US Index.

How the lifecycle works

The returns listed in the table above show clearly how lifecycles operate: the level of risk is reduced as you get closer to the retirement age. This is because the window of time left to offset shocks in the financial markets diminishes progressively. During this stage, investment risk and interest-rate risk are pared down by anchoring portfolios with bonds. One of the factors that makes bonds valuable is their stability: they are less volatile than stocks, meaning they tend to hold up better in weak markets but don’t perform as well in strong markets. This ensures that the impact of shocks in the financial markets (caused, in this case, by the COVID-19 pandemic) is reduced as you start approaching the retirement age.

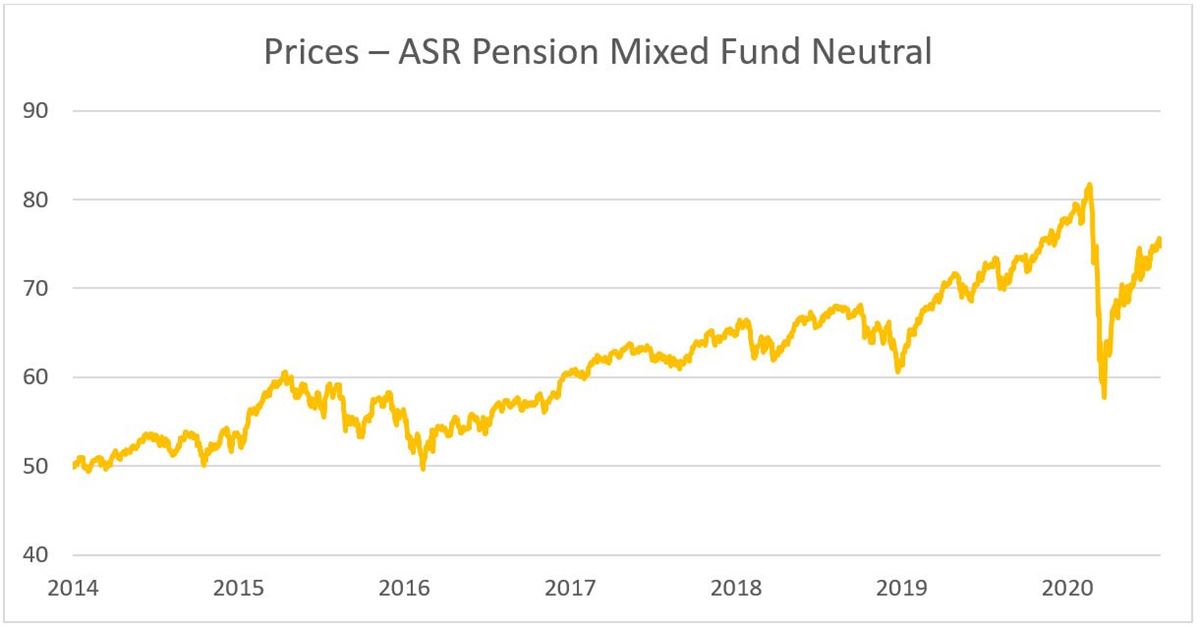

Long term

Judging by price trends for the ASR Pension Mixed Fund Neutral (consisting of stocks and bonds) since the fund was created in late 2013, we have yet to fully recover from the March 2020 slump. While we note that the outlook for the future is slightly less positive than before March, knowing that stock markets have always bounced back from financial crises in the past it is important not to lose sight of the long term. Net annualised return (NAR) for ASR Pension Mixed Fund Neutral has been +7.25% since the fund’s creation in 2013.

Outlook

Although we expect economic growth recovery to persist over the next few months, we assume this growth will be more moderate than the current rate, with the coronavirus continuing to spread worldwide. There is also the reality that a second wave of the pandemic later this year cannot be ruled out as long as there is no vaccine and/or medication available.

Financial markets – notably the more high-risk asset classes – already began their ascent in the past quarter, ahead of the current growth witnessed in the wider economy. Markets have yet to fully recoup their first-quarter losses, with stocks in particular appearing to be expensive rather than low-priced due to a combination of higher share prices and lower corporate profits. Corporate bonds are currently more appealing, with the added advantage that the ECB is set to continue buying billions of euros worth of these bonds in the foreseeable future. Interest rates on government bonds appear to be essentially low, owing to the combination of the improved economic outlook and the long-term rise in public debt. We believe the current precarious outlook calls for a restrained strategic positioning within the mixed funds overall, with marginally overweight corporate bonds and slightly underweight government bonds.

The investment returns shown on this page have been carefully prepared by a.s.r. Errors and omissions excepted.